You earn money. You spend money. But do you actually know where it all goes? Most people don't — and that's the number one reason budgets fail.

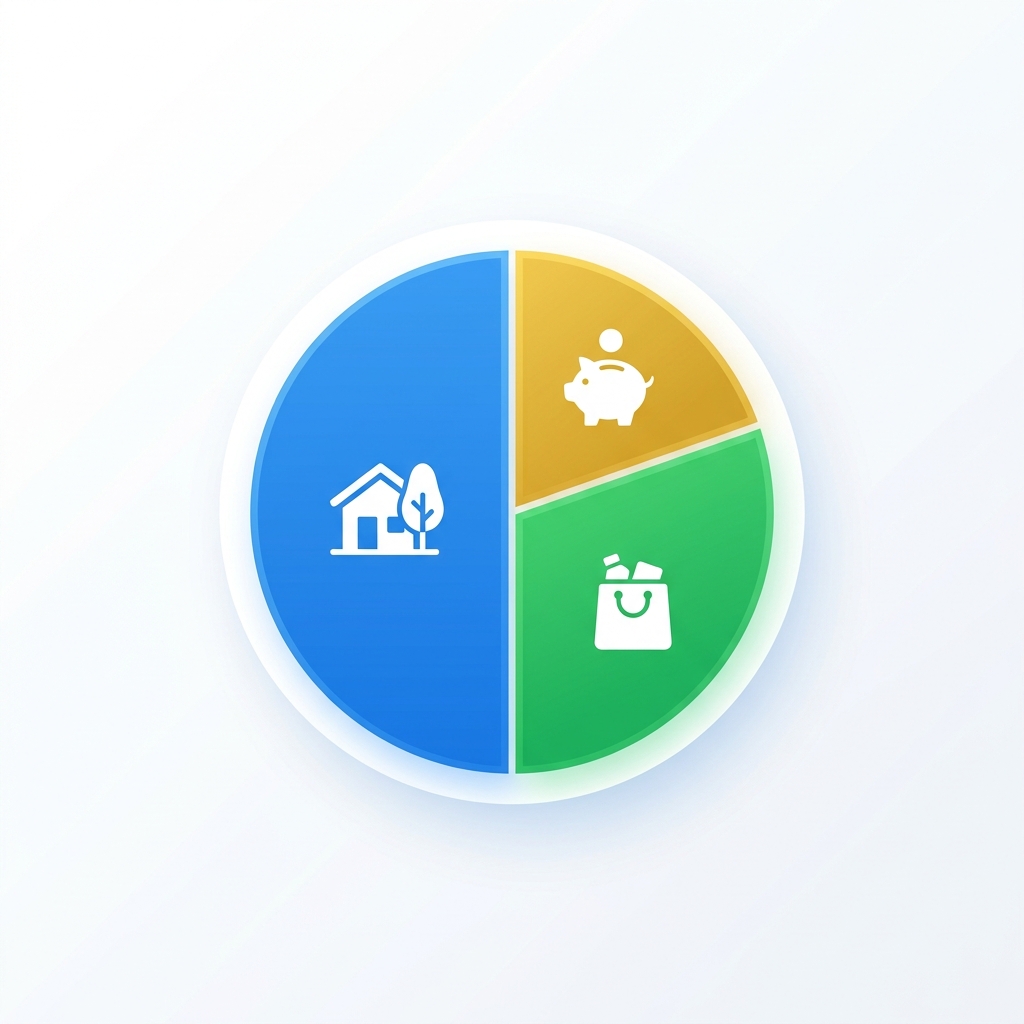

The 50/30/20 rule fixes that problem. It's the simplest budgeting framework ever created, and it works because it doesn't ask you to track every single coffee purchase. Instead, it splits your take-home pay into three buckets: needs, wants, and savings.

Here's how to set it up in under 10 minutes — and why it might be the only budget you'll ever stick to.

How the 50/30/20 Rule Works

Take your monthly after-tax income (what hits your bank account) and divide it like this:

| Category | % of Income | What It Covers |

|---|---|---|

| Needs | 50% | Rent, groceries, utilities, insurance, minimum debt payments |

| Wants | 30% | Dining out, streaming, hobbies, travel, shopping |

| Savings & Debt | 20% | Emergency fund, retirement, investments, extra debt payments |

That's it. Three numbers. No spreadsheet with 47 categories. No guilt about buying a latte.

Real Example: $5,000 Monthly Take-Home

Let's say you bring home $5,000 per month after taxes. Here's what your 50/30/20 budget looks like:

| Category | Budget | Typical Breakdown |

|---|---|---|

| Needs (50%) | $2,500 | Rent $1,400 + Groceries $400 + Car payment $300 + Insurance $250 + Utilities $150 |

| Wants (30%) | $1,500 | Dining out $300 + Streaming $50 + Gym $50 + Shopping $400 + Travel fund $400 + Entertainment $300 |

| Savings (20%) | $1,000 | Emergency fund $400 + 401(k) $400 + Extra on student loan $200 |

What this means for you: If you're saving $1,000 a month, that's $12,000 a year — enough to build a solid emergency fund in 6 months and still invest for retirement. Use our Savings Goal Calculator to see exactly when you'll hit your target.

Step-by-Step: Set Up Your 50/30/20 Budget

Step 1: Calculate Your After-Tax Income

Look at your last paycheck. Your net pay (after taxes and deductions) is your starting number. If you're self-employed, take your gross income minus estimated taxes.

Not sure about your take-home? Plug your salary into our Tax Calculator to get your net income.

Step 2: List Your "Needs"

These are expenses you literally can't avoid:

- 🏠 Housing — rent or mortgage (including property tax and insurance)

- 🛒 Groceries — food you cook at home (not restaurants)

- ⚡ Utilities — electricity, water, gas, internet

- 🚗 Transportation — car payment, gas, public transit

- 🏥 Insurance — health, auto, renter's/homeowner's

- 💳 Minimum debt payments — student loans, credit cards, car loans

Pro tip: If your needs exceed 50%, you likely need to reduce housing costs or find cheaper insurance. This is the hardest category to cut — but also the one that makes the biggest difference.

Step 3: Identify Your "Wants"

Wants are things you enjoy but could survive without:

- 🍽️ Restaurants and takeout

- 📺 Netflix, Spotify, subscriptions

- 🏋️ Gym memberships

- ✈️ Travel and vacations

- 🛍️ Clothes, gadgets, non-essential shopping

- 🎮 Gaming, concerts, entertainment

The line between "need" and "want" can get blurry. A phone is a need. The latest iPhone Pro Max is a want. Basic internet is a need. The premium 1Gbps plan might be a want.

Step 4: Automate Your Savings

The 20% savings bucket is where the magic happens. Set up automatic transfers on payday so you never have to think about it:

- 💰 Emergency fund first — aim for 3-6 months of expenses. Use our Savings Calculator to set a target.

- 📈 Retirement next — maximize your 401(k) match, then add to an IRA. See how your money grows with our Retirement Calculator.

- 💳 Extra debt payments — throw the rest at your highest-interest debt. Our Loan Calculator shows exactly how much interest you'll save.

When the 50/30/20 Rule Doesn't Work

Let's be honest. This rule was created when housing was affordable. In 2026, many people spend 40-60% of their income on rent alone. If that's you, here are adjusted versions:

| Your Situation | Adjusted Split | Why It Works |

|---|---|---|

| High-cost city (NYC, SF, LA) | 60/20/20 | Accepts higher needs, cuts wants by 10% |

| Aggressive debt payoff | 50/20/30 | Shifts 10% from wants to extra debt payments |

| Low income, building savings | 70/20/10 | Focuses on basics while saving even a small amount |

| High earner, FIRE goal | 30/20/50 | Maximizes savings and investments |

The point isn't hitting exactly 50/30/20. The point is having a framework — any framework — that forces you to allocate money intentionally instead of wondering where it all went.

50/30/20 vs Other Budget Methods

| Method | Difficulty | Best For | Drawback |

|---|---|---|---|

| 50/30/20 | Easy | Most people — simple, flexible | May not work in high-cost areas |

| Zero-based | Hard | Detail-oriented people | Every dollar assigned — tedious to maintain |

| Envelope system | Medium | Overspenders who need physical limits | Impractical for digital payments |

| Pay yourself first | Easy | People who only care about savings rate | No structure for spending categories |

Frequently Asked Questions

Does the 50/30/20 rule use gross or net income?

Net income — your take-home pay after taxes and mandatory deductions. If you contribute to a 401(k) through payroll, you can include that as part of your 20% savings.

What if my rent alone is more than 50% of my income?

Adjust the percentages. A 60/20/20 or even 70/20/10 split is perfectly fine as a starting point. The key is to save something consistently, even if it's only 10%.

Where do student loan payments go — needs or savings?

Minimum payments go in "needs" (they're mandatory). Any extra payments beyond the minimum go in "savings/debt repayment." Use our Student Loan Calculator to see how extra payments shorten your payoff date.

Is the 50/30/20 rule good for high earners?

It's a starting point, but high earners should aim to save more than 20%. Once your needs are met, shift extra income to investments rather than inflating your "wants" category. A 30/20/50 split lets you build wealth faster.

How do I track my spending?

You don't need to track every dollar. Just review your bank statement once a month and sort transactions into three columns: needs, wants, savings. If any category is way off, adjust next month.