Closing costs are the fees, taxes, and prepaid items you pay on top of your down payment when a home sale finalizes. Learning how to calculate closing costs before you make an offer can save you thousands — and prevent the sticker shock that hits many buyers three days before closing when the lender sends over the Closing Disclosure.

For a typical 2026 purchase, expect closing costs of roughly 2% to 5% of the loan amount for the buyer. On a $400,000 home with a $360,000 loan, that is $7,200 to $18,000 in addition to your down payment. Here is exactly what makes up that number, how to estimate it before you apply, and where you can shop around to shrink it.

Quick Answer: How to Calculate Closing Costs

- Start with your loan amount (purchase price minus down payment).

- Multiply by 3% as a mid-range national estimate for lender and third-party fees.

- Add prepaid items: roughly 2–6 months of property taxes, 12 months of homeowners insurance, and 15 days of mortgage interest.

- Add state and local transfer taxes if your state charges them (a handful do not).

- Subtract any seller concessions or lender credits you have negotiated.

The result is a realistic cash-to-close figure. For precise numbers on your specific loan, plug them into our free mortgage calculator and then layer closing costs on top of the monthly payment estimate.

What Are Closing Costs, Really?

Closing costs fall into two buckets that people often mix up. The first is true fees paid to the lender, title company, appraiser, and government — money you will not see again. The second is prepaid items, which are advance deposits for property tax and insurance escrows. Prepaids feel like a cost because they leave your bank account at closing, but they are really just early payments for bills you were going to owe anyway.

According to 2026 data, average closing costs on a $350,000 home are about $6,900 excluding transfer taxes, and roughly $10,300 including them. National costs rose 3.8% between 2025 and 2026 as home values and title premiums increased.

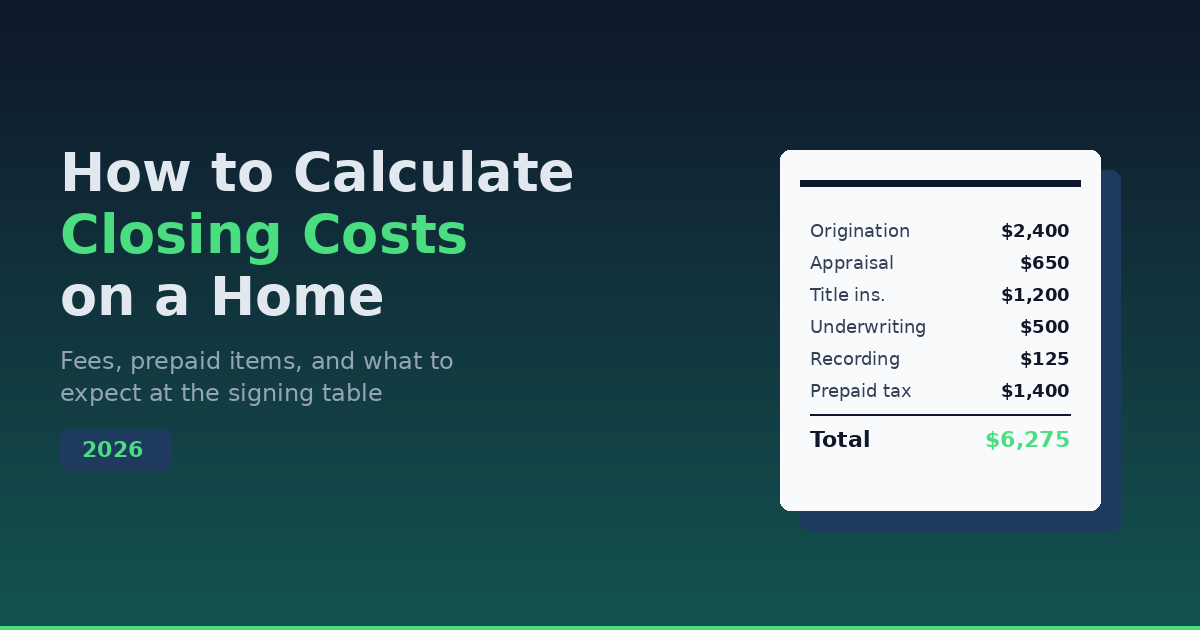

Line-by-Line: The 2026 Closing Cost Breakdown

Below is a realistic breakdown for a conventional 30-year loan on a $400,000 home with 10% down ($360,000 loan). Your numbers will shift with your state, lender, and credit profile.

| Line Item | Who Charges It | Typical Cost (2026) |

|---|---|---|

| Loan origination fee | Lender | 0% – 1% of loan ($0 – $3,600) |

| Underwriting fee | Lender | $300 – $750 |

| Processing fee | Lender | $300 – $900 |

| Credit report | Lender | $35 – $80 |

| Discount points (optional) | Lender | 1% per point ($3,600 each) |

| Appraisal | Third party | $500 – $1,000 |

| Home inspection | Third party | $350 – $600 |

| Title search and lender''s title insurance | Title company | $300 – $2,500 |

| Owner''s title insurance (optional but recommended) | Title company | $500 – $2,000 |

| Survey (where required) | Third party | $350 – $600 |

| Recording fee | Local government | $50 – $250 |

| Transfer tax | State/local government | 0% – 2% of price |

| Prepaid property tax (2–6 months) | Escrow | $800 – $3,000 |

| Prepaid homeowners insurance (12 months) | Escrow | $1,200 – $2,500 |

| Prepaid interest (mid-month closings) | Lender | $200 – $900 |

Lender Fees

Lender fees are the most shoppable piece of the stack. Origination charges alone ranged from $0 to $12,000+ on 2025 conforming loans, with a median of 0.66% of the loan amount per HMDA data. If one lender quotes a 1% origination fee and another quotes none, that is a real $3,600 difference on a $360,000 loan. Get at least three Loan Estimates within a two-week window and compare the top section side by side.

Third-Party Fees

You pay for the appraisal, inspection, and title work, but you do not always get to choose the provider. The Loan Estimate identifies which services you can shop for — title insurance is the big one. The American Land Title Association notes premiums can vary by up to 50% between providers in the same market, a spread worth roughly $750 on a $400,000 home.

Prepaid Items and Escrow

Lenders collect 2–6 months of property tax and 12 months of homeowners insurance up front to seed your escrow account. Prepaid interest covers the days from closing to the end of the month, so closing on the 28th is cheaper than closing on the 2nd. These are not negotiable, but timing your closing date near month-end can trim a few hundred dollars in interest.

Government Fees

Recording fees are small and fixed. Transfer taxes are not. Pennsylvania, New York, and Delaware charge some of the highest rates in the country, while 13 states — including Texas, Missouri, and Wyoming — charge no state-level transfer tax at all. Check your state and county before assuming a national average.

A Worked Example: $400,000 Home in Ohio

Let''s walk through a realistic scenario. A first-time buyer purchases a $400,000 home in Ohio with 10% down on a 30-year conventional loan at 6.75%.

- Loan amount: $360,000

- Origination fee (0.5%): $1,800

- Underwriting + processing + credit: $950

- Appraisal: $650

- Home inspection: $450

- Lender''s title insurance: $900

- Owner''s title insurance: $1,100

- Recording fee: $125

- Ohio conveyance fee (0.4%): $1,600

- Prepaid property tax (3 months, ~1.5% rate): $1,500

- Prepaid homeowners insurance (12 months): $1,600

- Prepaid interest (15 days): $1,000

Total cash to close: roughly $11,675 in closing costs plus the $40,000 down payment = $51,675. That is about 2.9% of the purchase price in closing costs — right in the middle of the typical range.

How to Reduce Closing Costs

Closing costs are more negotiable than most buyers realize. Five moves that actually move the number:

- Negotiate seller concessions. In a balanced or buyer-leaning market, asking the seller to cover 2–3% of closing costs is common. Conventional loans cap concessions at 3% with less than 10% down, 6% with 10–25% down.

- Shop title insurance. Request quotes from two or three title companies. A $500–$1,500 swing is realistic.

- Compare three Loan Estimates. Apply with multiple lenders within 14 days so credit inquiries count as one under FICO scoring. Use the offers to negotiate.

- Accept a lender credit. A slightly higher interest rate in exchange for a credit at closing can make sense if you plan to refinance or move within 5 years.

- Close near the end of the month. Closing on the 28th instead of the 3rd cuts prepaid interest substantially.

- Check for first-time buyer programs. Many state housing finance agencies offer closing cost assistance grants of $5,000–$10,000 for qualifying buyers.

When You Get the Numbers: Loan Estimate vs Closing Disclosure

Federal law gives you two checkpoints. Within three business days of applying, lenders must send a standardized three-page Loan Estimate. At least three business days before closing, you receive the five-page Closing Disclosure. Compare them line by line. Fees in the "Services You Cannot Shop For" section cannot increase more than 10% in aggregate, and lender fees generally cannot change at all. If they did, ask why — lenders are legally required to issue a corrected disclosure and restart the 3-day clock.

Rolling Closing Costs Into Your Loan

On a refinance, you can often roll closing costs into the new loan balance. On a purchase, you generally cannot — but you can take a lender credit that covers them in exchange for a rate bump of roughly 0.25%. On a $360,000 loan, a 0.25% rate increase adds about $55 a month or $19,800 over 30 years. Rolling $8,000 of closing costs into that credit only makes sense if you will move or refinance before crossing the break-even point, which is typically 5–7 years. Run both scenarios through our refinance calculator if you are considering this tradeoff.

Cross-References

For more context on the full home-buying math, see our guides on how much down payment you need in 2026 and how much house you can afford. Both work hand-in-hand with closing cost planning.

Ready to Run the Numbers?

Estimate your full monthly payment — principal, interest, taxes, and insurance — with MyCalcFinance''s free mortgage calculator. Then add 3% of the loan amount as a working closing cost estimate, refine it with quotes from three lenders, and you will walk into the closing table with no surprises.

FAQ

Are closing costs tax deductible?

Most are not. Mortgage interest and property taxes paid at closing are deductible if you itemize, as are discount points in the year you buy a primary home. Origination fees, appraisal, title insurance, and similar charges are not deductible but can be added to your home''s cost basis, reducing capital gains when you eventually sell.

Who pays closing costs, the buyer or the seller?

Both pay, but different line items. Buyers typically cover lender fees, appraisal, title insurance, and prepaid escrow. Sellers usually pay real estate agent commissions and owner''s title insurance in many states. Seller concessions toward buyer closing costs are common and often negotiated into the purchase agreement.

Can closing costs be paid with a credit card?

No. Lenders require certified funds — a cashier''s check or wire transfer — for the cash-to-close. Paying with a credit card would show up as new debt during the underwriting period and could derail the loan.

How accurate is the Loan Estimate?

Very accurate for lender fees, which cannot change at all except under specific circumstances. Services you cannot shop for cannot increase more than 10% in aggregate. Prepaid items and property taxes can change because they are based on real, external numbers.

Do VA and USDA loans have lower closing costs?

VA loans cap what the veteran can pay in closing costs and prohibit certain fees, which generally makes them cheaper. VA loans charge a one-time funding fee (1.25%–3.3% of the loan in 2026), but there is no monthly mortgage insurance. USDA loans carry a 1% upfront guarantee fee but keep other costs modest.