If you own a home, you're likely sitting on more wealth than you realize. As of the March 2026 ICE Mortgage Monitor, U.S. homeowners hold a record $17 trillion in total home equity, with about $11 trillion of that classified as "tappable" — money you could borrow against while still keeping a healthy 20% cushion in your home. The average mortgage holder has roughly $195,000 of tappable equity available right now.

The two most common ways to access that money are a home equity loan and a HELOC (home equity line of credit). They sound similar, share the same collateral (your house), and even use the same word — equity — but they behave very differently in your monthly budget. Picking the wrong one can cost you thousands of dollars in interest or trap you with a payment you can't predict.

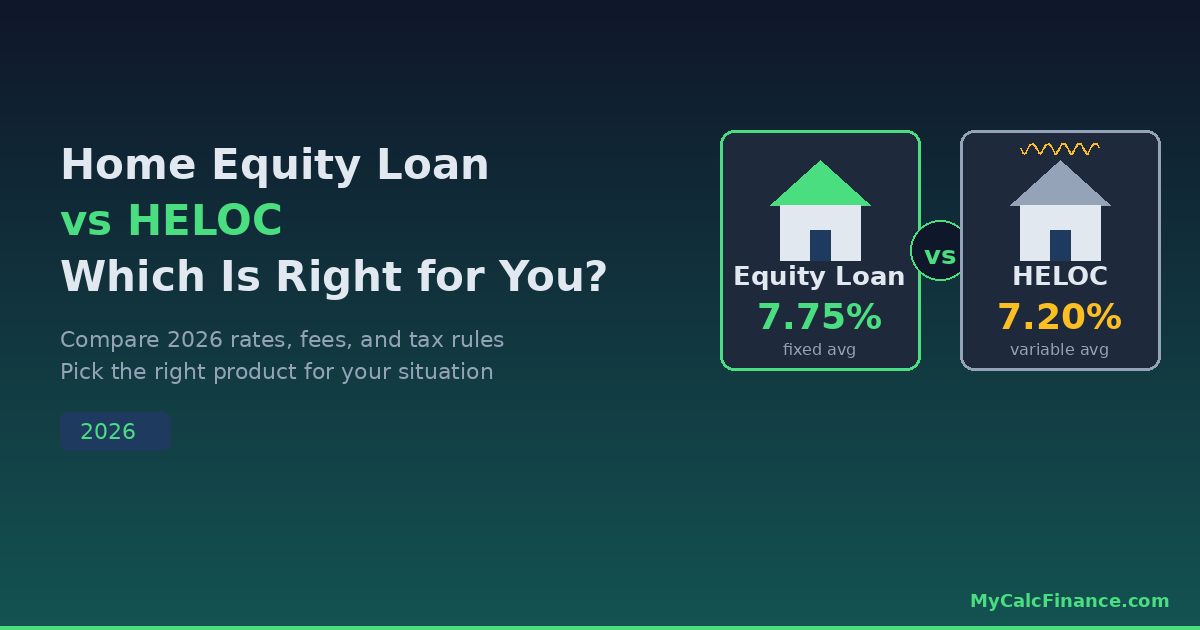

This guide breaks down the home equity loan vs HELOC decision with current 2026 rates, real numbers, the tax rules that actually apply, and a clear framework for choosing between them.

Quick Answer: Home Equity Loan vs HELOC

Here's the short version before we dig in:

- Home equity loan — One lump sum, fixed interest rate, fixed monthly payment. Best when you know exactly how much you need (kitchen remodel quote, debt consolidation balance, single tuition bill).

- HELOC — Revolving credit line you can draw from as needed, variable interest rate, interest-only payments allowed during the draw period. Best when expenses are spread out, uncertain, or recurring (multi-phase renovation, ongoing tuition, business cash flow).

As of mid-April 2026, the national average HELOC rate sits around 7.07%–7.24%, while the average home equity loan rate is roughly 7.37%–7.93% (Bankrate and Yahoo Finance data). The HELOC looks cheaper today — but that rate floats with the market, and history says it can move fast.

What Is a Home Equity Loan?

A home equity loan — sometimes called a "second mortgage" — gives you a single lump sum at closing, repaid in equal monthly installments over a fixed term (commonly 5, 10, 15, or 20 years) at a fixed interest rate.

The math works exactly like your primary mortgage: the lender amortizes the balance, and each payment chips away at both interest and principal until the loan is gone.

How Lenders Decide What You Can Borrow

Most lenders cap your combined loan-to-value (CLTV) at 80%–85%. CLTV is your total mortgage debt (first mortgage + home equity loan) divided by your home's appraised value.

Quick example: your home appraises at $500,000 and you owe $300,000 on your primary mortgage. At an 80% CLTV cap, the lender will let your total debt reach $400,000 — which means a maximum home equity loan of $100,000.

You can sanity-check what monthly payment that translates into using our free loan calculator before you ever fill out an application.

Pros of a Home Equity Loan

- Predictable payment. The rate is locked, so your monthly payment never changes.

- One-time discipline. You can't accidentally borrow more — when the lump sum is gone, it's gone.

- Longer terms available. Stretching to 15 or 20 years can keep payments low for big projects.

- Lower rate than personal loans or credit cards. Even at 7.5%–8%, it crushes the average credit card APR (over 21% in 2026).

Cons of a Home Equity Loan

- You start paying interest on day one — on the entire balance, even funds you haven't spent yet.

- Inflexible. Need a little more money next year? You'd have to apply for another loan.

- Closing costs. Expect to pay 2%–5% of the loan amount in fees (more on that below).

- Your home is collateral. Miss enough payments and the lender can foreclose.

What Is a HELOC?

A HELOC is a revolving credit line secured by your home. Think of it as a credit card with a much higher limit, a much lower interest rate, and your house on the line if you don't pay.

HELOCs have two distinct phases:

- Draw period (typically 5–10 years) — You can borrow, repay, and re-borrow up to your credit limit. Most lenders allow interest-only payments during this phase.

- Repayment period (typically 10–20 years) — The credit line closes. You make principal-and-interest payments to fully amortize the remaining balance, often at a higher monthly amount.

How HELOC Interest Actually Works

HELOC rates are almost always variable, tied to the Wall Street Journal Prime Rate plus a margin set by the lender. As of April 2026, prime is around 7.50%, so a HELOC priced at "prime + 0%" lands at roughly 7.50%, while "prime − 0.25%" lands near 7.25%.

If the Federal Reserve raises rates, your HELOC rate moves with it — usually within a single billing cycle. That's the trade-off for the flexibility.

Pros of a HELOC

- Pay interest only on what you use. A $50,000 line you haven't touched costs you nothing in interest.

- Reusable. Borrow $20,000 for a bathroom this year, pay it back, then borrow $30,000 for a roof in three years — no new application.

- Lower upfront costs. HELOC closing costs run 1%–5% of the credit limit, often on the lower end of that range, and many lenders waive them entirely.

- Cheaper rate today than a comparable home equity loan, as the current 2026 averages show.

Cons of a HELOC

- Variable rate risk. If prime climbs 2 percentage points, so does your rate — and your payment.

- Payment shock at the end of the draw period. Going from interest-only to fully amortizing can double or triple your monthly payment overnight.

- Temptation to overspend. An open credit line on your house is a different psychological beast than a one-time check.

- Annual or inactivity fees. Many HELOCs charge $50–$250/year, plus early-termination penalties of 2%–5% if you close in the first three years.

Side-by-Side Comparison

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| How you receive funds | Lump sum at closing | Draw as needed during 5–10 year window |

| Interest rate | Fixed (avg ~7.37%–7.93% in April 2026) | Variable (avg ~7.07%–7.24% in April 2026) |

| Monthly payment | Fixed principal + interest | Often interest-only during draw period |

| Term | 5–30 years, typically 10–20 | 5–10 year draw + 10–20 year repayment |

| Closing costs | 2%–5% of loan | 1%–5% of credit limit; often waived |

| Ongoing fees | None typical | $50–$250/year possible |

| Best for | Known, one-time expense | Ongoing or unpredictable expenses |

A Real Worked Example: $80,000 Borrowed

Let's compare both options side-by-side using a $80,000 borrowing need over 10 years. Home value: $600,000. First mortgage balance: $250,000. CLTV after the new loan: 55% — well within any lender's comfort zone.

Option A: Home equity loan at 7.75% fixed, 10-year term

- Monthly payment: $960

- Total interest over 10 years: $35,166

- Closing costs (assume 3%): $2,400

- True total cost: $37,566

Option B: HELOC at 7.20% variable, 10-year draw, then 10-year repayment

Assume you draw the full $80,000 immediately and the rate stays flat (it probably won't, but this is the optimistic case).

- Interest-only payment during draw: $480/month

- Total interest in years 1–10 (interest-only): $57,600

- If the balance is still $80,000 at the start of repayment, P&I jumps to about $938/month for years 11–20, costing another $32,560 in interest

- Closing costs (assume 1%): $800

- True total cost (worst case, never paying down principal): $90,960

The lesson: a HELOC's lower rate doesn't help if you only pay the minimum. The home equity loan forces discipline. The HELOC requires it. If you'd actually pay down the HELOC at the same $960/month the home equity loan demands, you'd save a few thousand dollars at today's rate spread — but only if rates stay flat. One full percentage point of rate increase (a 7.20% → 8.20% move) wipes out that advantage entirely.

Tax Deductibility in 2026: The Rule That Trips People Up

Under current IRS rules, interest on a home equity loan or HELOC is only tax-deductible when the borrowed money is used to "buy, build, or substantially improve" the home that secures the loan. The deduction is also subject to the combined $750,000 mortgage debt cap (for loans taken after December 15, 2017; $1 million for older loans).

Translation: borrow $50,000 to add a primary suite — interest is deductible. Borrow the same $50,000 to consolidate credit card debt, pay tuition, or fund a wedding — interest is not deductible, even though the loan itself is identical.

Save your receipts. The IRS expects documentation showing the funds went into the home if you claim the deduction. And even when the interest qualifies, you only benefit if your total itemized deductions exceed the standard deduction ($15,000 single / $30,000 married filing jointly in 2025 — adjust for the 2026 inflation-indexed figure when filing).

How to Choose: A Decision Framework

Pick a Home Equity Loan if…

- You know the exact dollar amount you need.

- You want a payment that won't change for the next 10–20 years.

- You're consolidating debt and need the structure of a forced payoff date.

- You believe rates will rise and want to lock in today.

- You'd be tempted to keep tapping a credit line "just because."

Pick a HELOC if…

- Your project has multiple phases or unpredictable costs (renovation, business, ongoing tuition).

- You want a financial safety net you may never actually use.

- You can comfortably absorb a 1–3 percentage point rate increase.

- You're disciplined enough to pay more than the interest-only minimum.

- You want to minimize upfront closing costs.

Consider a Cash-Out Refinance Instead if…

- Your current first mortgage rate is at or above today's market rates.

- You need a very large amount (often $100,000+) and want the longest possible term.

- Read our guide on whether to refinance your mortgage in 2026 for the full math.

Qualifying in 2026: What Lenders Want to See

Both products use roughly the same underwriting criteria:

- Credit score: 680 minimum at most lenders; 740+ unlocks the best rates.

- Debt-to-income ratio: Generally 43% or lower, including the new loan payment.

- Equity: At least 15%–20% remaining after the new loan (CLTV ≤ 80%–85%).

- Verifiable income: W-2s, pay stubs, or two years of self-employment tax returns.

If your score isn't where you want it, hold off and run the playbook in our guide on improving your credit score before borrowing against your house. A 40-point bump can drop your rate by half a percentage point or more — easily $5,000+ in lifetime interest on an $80,000 loan.

Closing Costs You'll Actually Pay

Both loan types carry closing costs that look a lot like a mini-mortgage:

- Appraisal: $300–$700 (some lenders use automated valuations and waive it)

- Origination fee: 0.5%–1% of the loan amount

- Title search and insurance: 0.1%–2% of the loan

- Credit report fee: $20–$50 (the CFPB has flagged sharp increases here in 2026 — ask upfront)

- Recording and notary fees: $50–$250

"No closing cost" HELOCs do exist, but the lender typically recoups the cost through a slightly higher rate or a 2%–5% early-termination fee if you close the line within 3 years. Always ask for the all-in APR, not just the headline rate.

Common Mistakes to Avoid

- Treating a HELOC like an ATM. The flexibility is the trap. Set a written rule for what the line is for before you sign.

- Ignoring payment shock. Calculate what your HELOC payment will look like during the repayment period — not just the draw period.

- Borrowing to chase the market. Tapping equity to invest in stocks or crypto puts your house on the line for an asset that can drop 30%+ in a bad year.

- Skipping the rate-shop. Credit unions and online lenders often beat big banks by 0.5%–1.0% on home equity products. Get at least three quotes within a 14-day window so the credit pulls count as one inquiry.

- Forgetting the tax test. Don't assume the interest is deductible. Ask whether the use qualifies under the buy/build/improve standard.

The Bottom Line

A home equity loan is the right tool when you know exactly how much you need, want a fixed payment, and value certainty over flexibility. A HELOC wins when your costs are spread out or uncertain, you want a financial safety net, and you can stomach a variable rate.

Either way, you're putting your house on the line — so the decision deserves real math, not a gut feel. Plug your numbers into our free loan calculator to compare monthly payments and total interest before you commit. A 30-minute spreadsheet today can save you tens of thousands over the next decade.

Frequently Asked Questions

Can I have both a home equity loan and a HELOC at the same time?

Yes, as long as your combined loan-to-value stays within the lender's limit (usually 80%–85%). Some homeowners use a small home equity loan to lock in a fixed payment for a known expense and a HELOC as a separate emergency reserve. Just remember: every dollar of additional debt against your home raises your foreclosure risk.

What credit score do I need for the best HELOC or home equity loan rate?

Most top-tier rates require a FICO score of 740 or higher. Lenders will work with scores as low as 680, but expect a rate that's 0.50%–1.50% higher. Below 680, options narrow quickly and rates can push into the 9%–11% range.

How long does it take to get approved?

Plan on 2–6 weeks from application to funding. The bottleneck is usually the appraisal — automated valuations cut that to 1–2 weeks. HELOCs sometimes close faster than home equity loans because some lenders skip a full appraisal on lower loan amounts.

Can the lender freeze or reduce my HELOC?

Yes. If your home value drops sharply, your credit score plunges, or the lender's risk model changes, they can suspend or reduce your line — even if you've never missed a payment. This happened widely during the 2008 crisis and again briefly in 2020. Don't treat an unused HELOC as a guaranteed emergency fund.

What happens if I sell my house with an outstanding home equity loan or HELOC?

Both must be paid off at closing from the sale proceeds, just like your first mortgage. If you owe more than the home is worth (after combining first mortgage + equity loan), you'd need to bring cash to closing or negotiate a short sale with the lenders.

Is a personal loan ever a better choice than a HELOC or home equity loan?

For amounts under $25,000 or short payback periods (1–5 years), a personal loan can be cheaper once you factor in closing costs — and your home isn't on the line. Run the all-in cost both ways before assuming "home equity is always cheapest."